After an accident, storm damage claim, house fire, water leak, or other insurance loss, one of the first people you may hear from is an insurance adjuster.

While many adjusters are professional and helpful, it is important to understand that the information you provide can affect your claim. Even innocent comments can sometimes be misunderstood or used to question damages, injuries, or liability.

If you’re currently dealing with a claim, you may also want to read our guide on what happens after you file an insurance claim to better understand the process from start to finish.

Below are ten things you should think carefully about before saying to an insurance adjuster.

1. “It Was My Fault”

One of the most common mistakes people make is admitting fault immediately after an accident.

The reality is that fault is often determined after reviewing evidence, witness statements, photographs, police reports, and other documentation. What seems obvious in the moment may not reflect the complete picture.

Instead of admitting blame, focus on providing accurate facts about what happened.

If you were involved in a vehicle accident, having video evidence can be incredibly valuable. A dash camera can often provide a clearer account of events than memory alone.

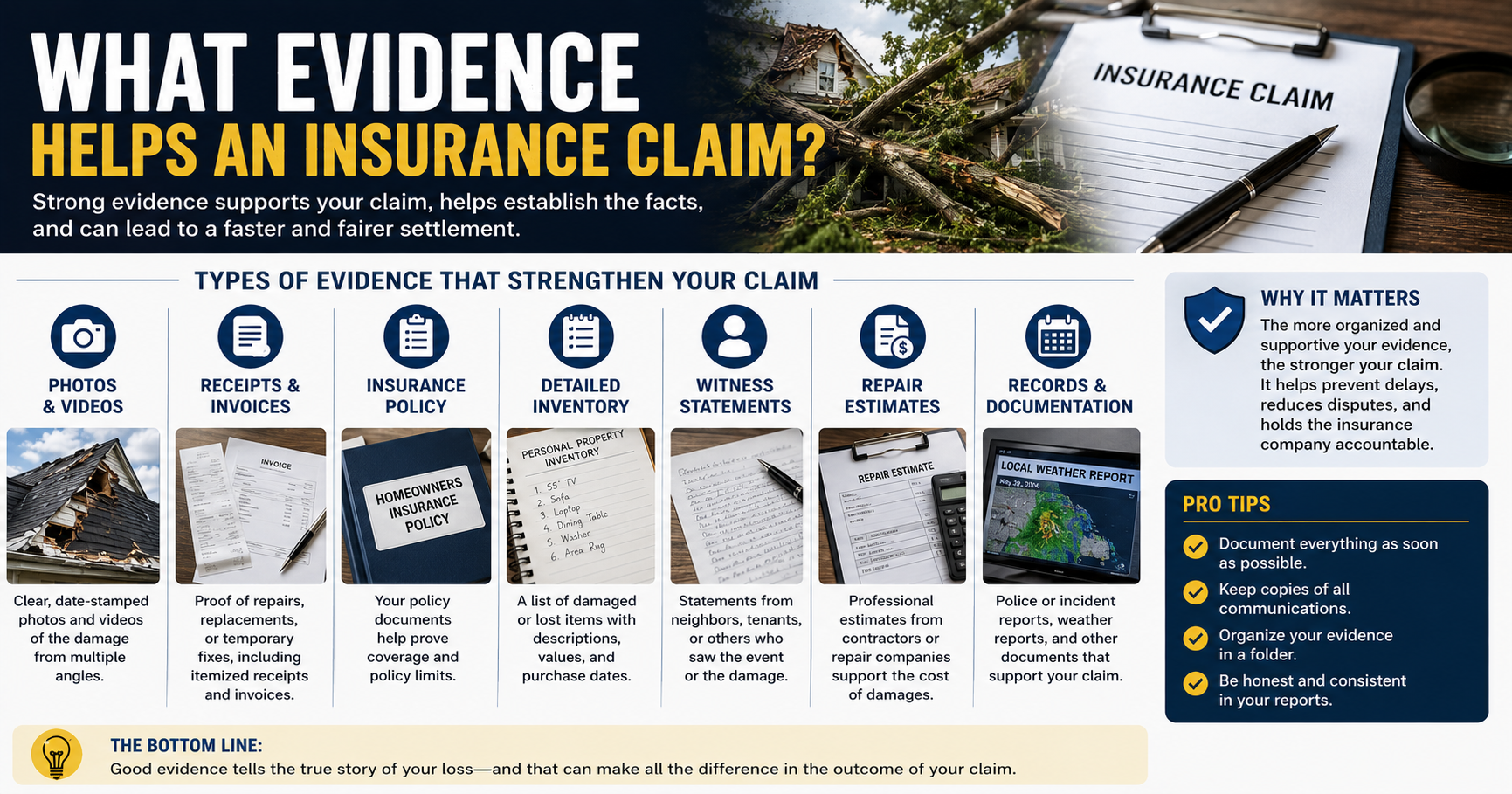

You may also be interested in reading what evidence helps an insurance claim to learn what documentation can strengthen your case.

2. “I’m Not Injured”

Many people feel fine immediately after an accident because of adrenaline.

Hours or even days later, symptoms such as neck pain, back pain, headaches, dizziness, or other injuries may begin to appear.

Telling an adjuster that you are not injured before receiving medical evaluation could create problems later if symptoms develop.

A safer response may be:

“I am still being evaluated and do not yet know the full extent of any injuries.”

If your claim involves injuries caused by another party, you may also find our Personal Injury Law section helpful:

3. “I Don’t Have Proof”

Many people believe they have no evidence simply because they did not take photographs immediately after an incident.

Evidence can come from many sources, including:

- Photographs

- Video recordings

- Witness statements

- Repair estimates

- Medical records

- Police reports

- Security camera footage

In fact, gathering evidence is one of the most important parts of the claims process.

Our article on can an insurance company deny a claim without investigation explains why evidence often becomes critical when disputes arise.

4. “It Wasn’t a Big Deal”

Many people try to be polite or avoid making a situation sound serious.

Unfortunately, minimizing damages can sometimes hurt your claim.

If a vehicle suffered major damage, a roof sustained storm losses, or water damage spread through a home, describing it as “not a big deal” may create unnecessary questions later.

Stick to facts rather than opinions.

Photographs, estimates, invoices, and inspection reports are usually far more helpful than personal opinions regarding the severity of damages.

5. “I Was in a Hurry”

Statements about rushing, being distracted, running late, or multitasking may unintentionally create questions about negligence.

Even if you believe the statement is harmless, it may become part of the claim file.

Instead, focus on describing the sequence of events without adding unnecessary commentary.

You may also want to read why do insurance companies deny claims to understand how seemingly small details sometimes affect claim decisions.

6. “I Don’t Remember”

There is nothing wrong with honestly saying you do not remember a specific detail.

The mistake happens when people start guessing.

Insurance claims often involve recorded conversations, written statements, photographs, witness interviews, repair estimates, and other evidence. If you guess incorrectly, that statement could later conflict with documented facts.

A better response is:

“I don’t recall that detail right now. I’d like to review my records before answering.”

Keeping organized records can make a huge difference during the claims process. Many people scan and save claim documents, receipts, estimates, and correspondence so they can easily access them later.

If you’re dealing with a delayed claim, you may also want to read how long does an insurance company have to respond to better understand typical claim timelines.

7. “Whatever You Think Is Fair”

Many people assume the insurance company will automatically offer the full value of their losses.

While adjusters work within company guidelines and policy limits, it is still important to understand the value of your damages before accepting any settlement.

Repair costs, replacement values, medical expenses, lost wages, and other damages should all be considered.

Never agree to a settlement simply because it sounds reasonable at first glance.

You should fully understand your losses before accepting any payment.

You may also find our Insurance Claims category helpful:

8. “I Don’t Need Records”

This is one of the biggest mistakes claimants make.

The more documentation you have, the stronger your claim often becomes.

Important records may include:

- Claim numbers

- Repair estimates

- Medical bills

- Receipts

- Photographs

- Emails

- Text messages

- Police reports

- Contractor invoices

- Correspondence with the insurance company

Many claim disputes happen months after the original incident.

Without documentation, it can become difficult to prove what was said, submitted, or agreed upon.

This is one reason many homeowners store important paperwork in fireproof storage containers and create digital backups of critical records.

9. “I’ll Sign Anything”

Never sign documents without reading and understanding them.

Insurance paperwork may include:

- Settlement agreements

- Releases of liability

- Property damage releases

- Medical authorizations

- Sworn statements

Once certain documents are signed, it may be difficult or impossible to reverse the decision.

If something seems confusing or unclear, take time to review it carefully before signing.

In more complicated situations, consulting an attorney may be worth considering.

If your claim has already been denied, you may want to read can you sue an insurance company to learn about potential legal options.

10. “This Is My Final Statement”

Insurance claims often evolve over time.

Additional damages may be discovered.

Repair estimates may increase.

Medical treatment may continue.

New witnesses may come forward.

Security footage may become available.

Because of this, avoid making absolute statements that suggest nothing could ever change.

Instead, provide accurate information based on what you know at the time.

If additional information becomes available later, you can update the claim accordingly.

Why Insurance Companies Pay Close Attention to Statements

Insurance companies rely heavily on statements when investigating claims.

Adjusters often compare:

- Recorded statements

- Written statements

- Photographs

- Medical records

- Repair invoices

- Witness accounts

- Police reports

Any inconsistency may raise questions that delay the claim process.

This does not mean you should be afraid to speak with an adjuster.

It simply means you should communicate carefully, honestly, and accurately.

What Should You Say to an Insurance Adjuster Instead?

A good rule is to focus on facts rather than opinions.

Instead of guessing, speculating, or exaggerating, simply explain:

- What happened

- When it happened

- Where it happened

- What damages occurred

- What evidence exists

If you are unsure about something, it is perfectly acceptable to say you need additional time to review records or gather information.

When Should You Consider Speaking With an Attorney?

Not every insurance claim requires legal help.

However, legal guidance may be beneficial if:

- Your claim was denied.

- The insurance company is delaying payment.

- The settlement offer appears unfair.

- Serious injuries are involved.

- Significant property damage occurred.

- Liability is being disputed.

You may also want to learn more about what is insurance bad faith if you believe an insurance company is handling your claim improperly.

Learn More About Your Legal Rights

At Legal Know It All, our goal is to help consumers better understand their rights and responsibilities.

You can learn more about our standards by visiting our:

- About Us: https://legalknowitall.com/about-us/

- Editorial Policy: https://legalknowitall.com/editorial-policy/

- Fact-Checking Policy: https://legalknowitall.com/fact-checking-policy/

- FAQ: https://legalknowitall.com/faq/

You can also browse additional resources in our Legal Questions section:

Understanding what to say and what not to say during an insurance claim can help protect your rights, avoid misunderstandings, and put you in a stronger position throughout the claims process.

As an Amazon Associate we earn from qualifying purchases through some links in our articles. Learn more.