Getting an insurance claim denial can feel like a punch to the gut.

You’ve paid premiums, reported the loss, provided information, and waited for a decision.

Then a letter arrives saying the claim has been denied.

Many people immediately assume they have no options left.

That’s not always true.

A denial means the insurance company has decided not to pay all or part of the claim based on the information currently available and its interpretation of the policy.

However, a denial does not automatically mean the matter is permanently closed.

In some situations, additional evidence, clarification, reconsideration requests, complaints, or other actions may still be available.

Quick Answer

If an insurance claim is denied, the insurance company will typically provide an explanation for the decision. Depending on the circumstances, policyholders may be able to review the denial, provide additional evidence, request reconsideration, file a complaint, or explore other dispute-resolution options. The best next step often depends on why the claim was denied.

Why Insurance Claims Get Denied

Insurance companies deny claims for many different reasons.

Some denials are based on policy language.

Others involve missing information or disputes about the facts.

Common reasons include:

- Coverage exclusions

- Missed deadlines

- Insufficient evidence

- Policy lapses

- Disputed facts

- Incomplete documentation

- Damage not covered by the policy

Understanding the specific reason for the denial is often the most important first step.

Read the Denial Letter Carefully

Many people become upset and immediately focus on the word “denied.”

While that’s understandable, the explanation contained in the denial letter is extremely important.

The letter may explain:

- Why the claim was denied

- What policy provisions apply

- What evidence was reviewed

- Whether additional information may be submitted

The reason provided often determines what options are available next.

Not Every Denial Means the Insurance Company Did Something Wrong

This is important to understand.

A denial is not automatically evidence of bad faith or misconduct.

Insurance companies are allowed to deny claims when:

- Coverage does not apply

- Exclusions exist

- Evidence is insufficient

- Policy requirements are not met

The key issue is whether the company handled the claim appropriately and reasonably.

If you’re concerned about how the claim was handled, you may also want to read:

What Is Insurance Bad Faith? Common Examples Explained

Can a Denied Claim Be Reconsidered?

Sometimes.

Many people assume a denial is final.

That isn’t always the case.

New information may become available after the denial.

Examples include:

- Additional photographs

- Witness statements

- Medical records

- Repair estimates

- Expert opinions

In some situations, providing additional information may lead to further review.

Readers facing this situation may also find helpful information in:

Can You Reopen a Closed Insurance Claim?

What If the Insurance Company Never Properly Investigated?

One of the most common complaints from policyholders is that they believe the insurer denied the claim too quickly.

Questions often arise when people feel the company:

- Ignored evidence

- Failed to inspect damage

- Overlooked important facts

- Never requested information

For more information, see:

Can an Insurance Company Deny a Claim Without Investigation?

Strong Evidence Can Make a Difference

Evidence often plays a major role in claim disputes.

Helpful evidence may include:

- Photographs

- Videos

- Receipts

- Estimates

- Inspection reports

- Police reports

- Medical records

Our article 10 Types of Proof That Can Strengthen Your Insurance Claim Case discusses some of the most valuable forms of documentation.

For vehicle accidents, recorded footage can sometimes help resolve factual disputes.

Many drivers use the VNV Front and Rear Dash Cam for Accident Evidence because it records both the front and rear of the vehicle and may help preserve important evidence that becomes relevant during claim investigations.

Should You Contact the Insurance Company?

In many situations, yes.

Before escalating a dispute, it often makes sense to contact the insurer and ask questions.

Examples include:

- Why was the claim denied?

- What evidence was considered?

- Is additional information needed?

- Can the decision be reviewed?

Sometimes misunderstandings can be resolved through communication alone.

What If You Still Disagree With the Decision?

This is where many people begin exploring additional options.

The appropriate next step depends heavily on:

- The reason for the denial

- Available evidence

- Policy language

- State law

Some disputes are resolved through additional review.

Others may require more formal action.

Understanding the Reason for the Denial Is the Most Important Step

Many people immediately focus on what they should do next.

However, the most important step is usually understanding exactly why the claim was denied.

The reason for the denial often determines:

- Whether additional evidence may help

- Whether reconsideration is possible

- Whether a complaint may be appropriate

- Whether other dispute-resolution options exist

The clearer your understanding of the denial, the easier it becomes to determine the best path forward.

Can You Appeal an Insurance Claim Denial?

In many situations, policyholders can ask the insurance company to review a denial.

People often refer to this process as an appeal, reconsideration request, or claim review.

The exact process varies depending on the insurance company and the type of claim involved.

An appeal may be appropriate when:

- New evidence becomes available

- Important information was overlooked

- Errors are discovered

- Additional documentation can be provided

A denial does not always mean the discussion is over.

What Evidence Can Help After a Denial?

Strong evidence is often one of the most valuable tools a policyholder has.

Depending on the claim, useful evidence may include:

- Repair estimates

- Contractor reports

- Medical records

- Photographs

- Videos

- Witness statements

- Police reports

- Receipts

The more clearly the evidence supports the claim, the easier it may be for the insurance company to evaluate the situation.

If you’re gathering documentation, our article 10 Types of Proof That Can Strengthen Your Insurance Claim Caseprovides additional examples of evidence that may help support a claim.

Keep Every Document Related to the Claim

One mistake many people make is throwing away documents after receiving a denial.

Even if the claim appears finished, retaining records can be extremely important.

Consider keeping:

- Denial letters

- Emails

- Estimates

- Receipts

- Inspection reports

- Claim numbers

- Photographs

Many people choose to digitize important records using the Canon imageFORMULA Portable Document Scanner so copies remain available if questions arise later.

Others store claim paperwork in a SentrySafe Fireproof Waterproof Document Safe or an ENGPOW Fireproof Document Storage Box to help protect important records from fire, water, and accidental loss.

Can You File a Complaint Against an Insurance Company?

Sometimes a policyholder believes the issue is not merely the denial itself but how the claim was handled.

In those situations, filing a complaint may be an option.

Many states allow consumers to submit complaints regarding:

- Claim delays

- Communication problems

- Claim denials

- Claim handling concerns

- Regulatory issues

For a detailed explanation, see:

Can You File a Complaint Against an Insurance Company?

Can You Sue an Insurance Company?

In some situations, legal action may be considered.

Whether a lawsuit is appropriate depends on many factors, including:

- State law

- Policy language

- Available evidence

- The amount in dispute

- The reason for the denial

Not every claim denial leads to litigation.

Many disputes are resolved through communication, additional review, or other processes before a lawsuit becomes necessary.

For more information, see:

Can You Sue an Insurance Company?

What If You Believe the Insurance Company Acted Unfairly?

Some denied claims lead policyholders to question whether the company acted reasonably during the investigation.

Examples of concerns may include:

- Ignoring important evidence

- Failing to investigate

- Misrepresenting policy language

- Unreasonable delays

- Poor communication

These situations are sometimes associated with discussions about insurance bad faith.

You can learn more in:

What Is Insurance Bad Faith? Common Examples Explained

How Long Should You Keep Insurance Claim Records?

Many people ask this question after a claim is denied.

While record retention needs vary, it is generally wise to keep claim-related documentation for an extended period of time.

Important records often include:

- Claim correspondence

- Estimates

- Settlement documents

- Denial letters

- Photographs

- Receipts

Keeping organized records may make future disputes significantly easier to handle.

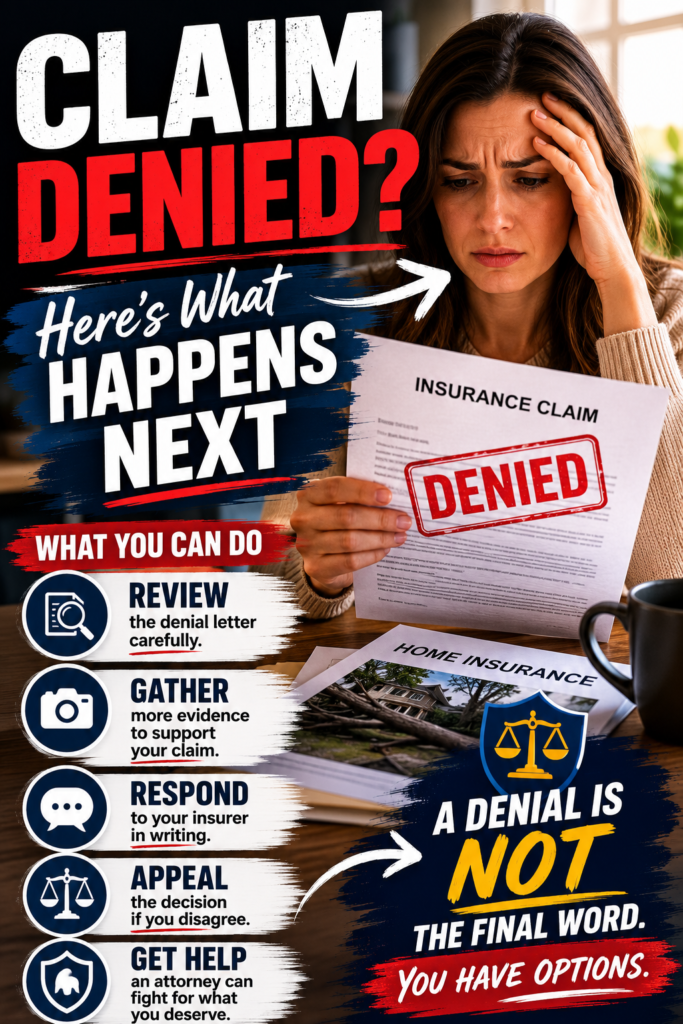

Practical Steps After a Claim Denial

If your claim has been denied, consider taking the following steps:

Read the Denial Letter

Understand the specific reason for the denial.

Review Your Policy

Look for the policy provisions referenced by the insurer.

Gather Evidence

Collect any additional documentation that may support your position.

Ask Questions

Request clarification if the explanation is unclear.

Stay Organized

Maintain copies of all claim-related records.

Evaluate Your Options

Depending on the circumstances, options may include reconsideration, complaints, additional review, or other dispute-resolution methods.

A Denial Is Not Always the End of the Story

Many people view a denied insurance claim as the end of the process.

In reality, some denied claims are later revisited because:

- New evidence becomes available

- Errors are corrected

- Additional information is provided

- Important facts are clarified

Understanding why the denial occurred is often the key to determining whether additional action may be worthwhile.

You may also find these related articles helpful:

- How Long Does an Insurance Claim Take? What to Expect

- What Happens After You File an Insurance Claim?

- What Happens After an Insurance Adjuster Visits?

- How Long Does an Insurance Company Have to Respond?

- Can an Insurance Company Deny a Claim Without Investigation?

- Can You Reopen a Closed Insurance Claim?

Frequently Asked Questions

Does a denied insurance claim mean I cannot receive compensation?

Not necessarily. A denial means the insurance company has decided not to pay the claim based on the information currently available and its interpretation of the policy. Depending on the circumstances, additional evidence or further review may still be possible.

Can I ask the insurance company to review the denial again?

In many situations, yes. Policyholders may sometimes request reconsideration or provide additional information that was not available during the original review.

How often are insurance claims denied?

Claim denials occur for many different reasons, including policy exclusions, insufficient evidence, missed deadlines, or disputes regarding the facts. The frequency varies depending on the type of insurance and claim involved.

What should I do first after receiving a denial letter?

Start by reading the denial letter carefully. Understanding the reason for the denial is often the most important step because it helps determine what options may be available moving forward.

Can new evidence help after a denial?

Sometimes. Photographs, videos, estimates, medical records, witness statements, and other documentation may provide information that was not previously available during the claim review process.

Can I file a complaint if I believe the denial was unfair?

In many states, yes. Consumers can often submit complaints to state insurance regulators regarding claim handling concerns, communication issues, delays, and other insurance-related disputes.

Can I sue an insurance company after a claim denial?

Sometimes. Whether legal action is appropriate depends on state law, policy language, available evidence, and the specific facts of the dispute.

What records should I keep after a claim denial?

It is generally a good idea to retain:

- Denial letters

- Claim correspondence

- Estimates

- Receipts

- Photographs

- Inspection reports

- Claim numbers

Many people choose to digitize records using the Canon imageFORMULA Portable Document Scanner and store important documents in a SentrySafe Fireproof Waterproof Document Safe for additional protection.

Can a denied claim be reopened later?

In some situations, yes. Newly discovered evidence, additional damage, administrative errors, or other factors may sometimes result in further review.

Where can I learn more about insurance claim disputes?

You may find these related guides helpful:

- What Happens After You File an Insurance Claim?

- Why Do Insurance Companies Delay Claims? Common Reasons

- What Is Insurance Bad Faith? Common Examples Explained

- Can You File a Complaint Against an Insurance Company?

- Can You Sue an Insurance Company?

Important Information

This article is provided for educational and informational purposes only and should not be considered legal advice. Insurance laws vary by state, insurance policies differ, and individual circumstances can significantly affect claim outcomes. Information provided on Legal Know It All is intended to help readers better understand insurance claim procedures and legal concepts, not to provide legal representation or legal advice.

To learn more about how content is researched and reviewed, visit our Editorial Policy and Fact-Checking Policy pages.

Additional information about this website can be found on our About Us, Contact Us, FAQ, Disclaimer, and Terms and Conditions pages.

About the Author

Sarah Reynolds is a legal research contributor for Legal Know It All who focuses on insurance claims, consumer rights, and everyday legal issues affecting American families. She researches insurance regulations, policyholder rights, claim procedures, and consumer-focused legal topics to help readers better understand complicated subjects using plain English. Her goal is to provide trustworthy educational information that helps readers make informed decisions when dealing with insurance companies and claim disputes.

As an Amazon Associate we earn from qualifying purchases through some links in our articles. Learn more.