Why Some Insurance Claims Get Reopened

Many people assume that once an insurance claim is closed, the matter is permanently finished.

That is not always true.

In some situations, policyholders discover additional damage, find missing documentation, uncover new evidence, or encounter other issues after a claim has already been closed.

When this happens, a common question is:

Can you reopen a closed insurance claim?

The answer depends on several factors, including the type of claim, the reason the claim was closed, the terms of the policy, and the laws that apply in your state.

Quick Answer

Sometimes a closed insurance claim can be reopened. Whether reopening is possible depends on factors such as the reason for closure, the type of claim, newly discovered evidence, additional damages, policy provisions, and applicable state laws. Not every closed claim can be reopened, but some claims may qualify for additional review.

What Does It Mean When a Claim Is Closed?

A closed claim generally means the insurance company considers its review of the matter complete.

Closure may occur after:

- A settlement payment

- A claim denial

- Completion of repairs

- Resolution of a dispute

- Lack of activity on the claim

However, a closed claim does not always mean every issue related to the loss has been permanently resolved.

The circumstances surrounding the closure matter.

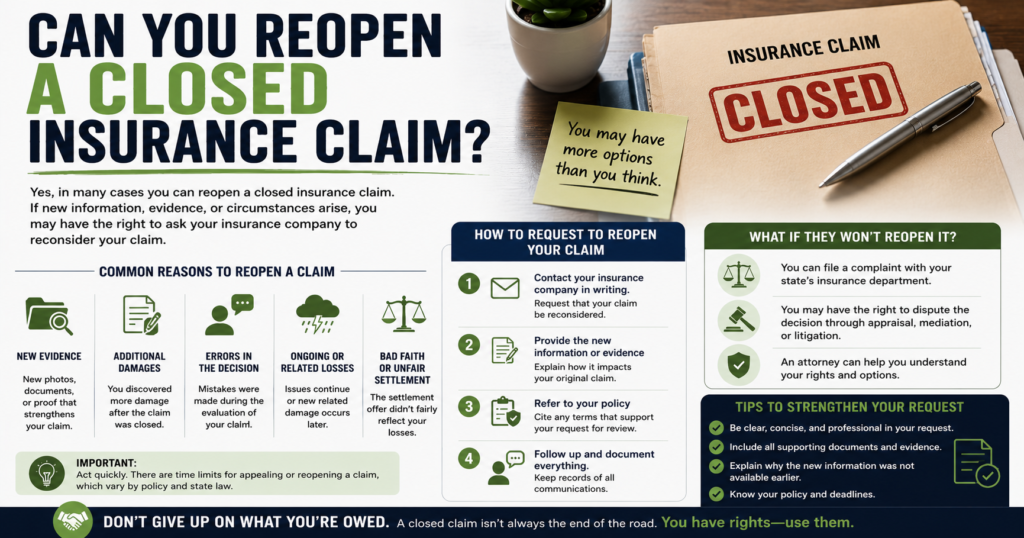

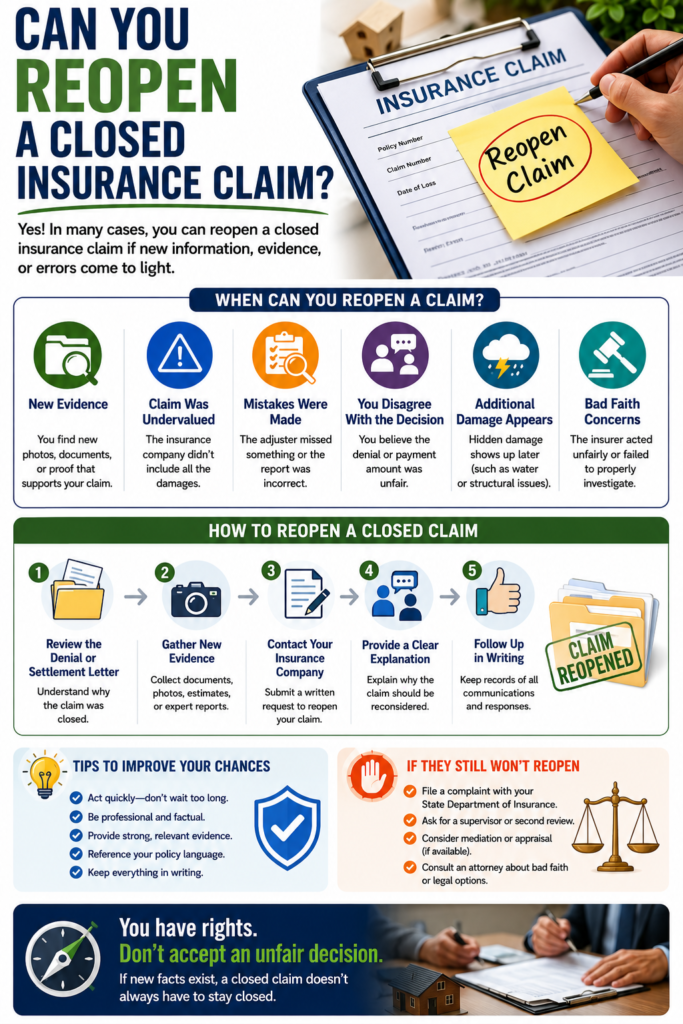

Common Reasons People Want to Reopen a Claim

There are several situations where policyholders seek additional review after a claim has already been closed.

Hidden Damage Was Discovered

This is one of the most common reasons.

For example:

A vehicle may appear fully repaired only for additional damage to be discovered later.

A home may suffer storm damage that is not fully visible during the initial inspection.

In these situations, new information may become available after the original claim review.

Additional Repairs Cost More Than Expected

Sometimes repair costs increase after work begins.

Contractors, mechanics, or specialists may uncover additional issues that were not obvious during the original estimate.

This can lead policyholders to ask whether the claim can be reviewed again.

New Evidence Becomes Available

Evidence plays an important role in many insurance decisions.

Examples may include:

- New photographs

- New videos

- Witness statements

- Repair reports

- Inspection findings

If important information was unavailable during the original investigation, a policyholder may want the insurer to review the claim again.

For a deeper look at claim documentation, see What Evidence Helps an Insurance Claim?.

Medical Conditions Become Worse

In some injury-related claims, symptoms may develop or worsen after the claim appears resolved.

These situations can be complex and often depend on the specific facts involved.

Does Reopening a Claim Mean Starting Over?

Usually not.

In many situations, the insurance company already has:

- Claim records

- Inspection reports

- Photographs

- Correspondence

- Previous decisions

As a result, reopening a claim often involves reviewing additional information rather than beginning the entire process from scratch.

Why Documentation Becomes Even More Important

The longer time passes after a claim closes, the more important documentation often becomes.

Helpful records may include:

- Settlement paperwork

- Estimates

- Inspection reports

- Repair invoices

- Photographs

- Emails

- Letters

Many policyholders create digital backups using a Canon imageFORMULA Portable Document Scanner so claim records remain organized and accessible if questions arise months or years later.

Can You Reopen a Denied Insurance Claim?

Sometimes.

However, reopening a denied claim often depends on why the denial occurred.

Examples that may prompt additional review include:

- New evidence

- Documentation errors

- Missing information

- Clarification of facts

The specific circumstances matter significantly.

If you’re dealing with a denial, you may also find helpful information in Can an Insurance Company Deny a Claim Without Investigation?.

What Role Does the Insurance Adjuster Play?

When additional review occurs, adjusters may once again become involved.

The adjuster may:

- Review new evidence

- Inspect additional damage

- Evaluate supplemental estimates

- Prepare updated reports

Depending on the situation, the insurance company may assign the original adjuster or another adjuster to review the matter.

For more information, see What Is an Insurance Adjuster? What They Actually Do.

Not Every Closed Claim Can Be Reopened

This is an important point.

Some policyholders assume reopening is always available.

That is not necessarily true.

Factors that may affect reopening include:

- State law

- Policy language

- Settlement agreements

- Claim type

- Available evidence

- Time elapsed since closure

Understanding these factors is often the first step in determining whether additional review may be possible.

What Is a Supplemental Insurance Claim?

One term that frequently appears when discussing reopened claims is “supplemental claim.”

A supplemental claim generally involves additional damages, expenses, or information that were not included during the original claim review.

For example:

- A contractor discovers hidden structural damage.

- A mechanic uncovers additional vehicle damage.

- Repairs cost significantly more than originally estimated.

- New documentation becomes available.

In some situations, a supplemental claim may be processed without requiring an entirely new claim.

The specific procedures vary by insurer and claim type.

Are There Time Limits for Reopening a Claim?

Sometimes.

Time limits can be affected by:

- Policy provisions

- State laws

- Settlement agreements

- Type of claim

- Type of damage

Because requirements vary, there is no single deadline that applies to every insurance claim.

This is one reason policyholders should avoid waiting longer than necessary when additional damages or evidence are discovered.

Reopening a Homeowners Insurance Claim

Homeowners claims are among the most common claims that may require additional review.

Examples include:

- Hidden water damage

- Storm damage discovered later

- Structural issues

- Mold concerns

- Roofing damage

Some forms of property damage may not be immediately visible during the first inspection.

When new issues are discovered, additional documentation often becomes extremely important.

Helpful evidence may include:

- New photographs

- Contractor reports

- Inspection reports

- Repair estimates

Reopening an Auto Insurance Claim

Vehicle claims may also be reopened in certain situations.

Examples include:

- Hidden frame damage

- Mechanical damage

- Supplemental repair estimates

- Newly discovered evidence

- Additional accident-related expenses

Vehicle repairs sometimes reveal problems that were not visible during the initial inspection.

This is one reason supplemental estimates are relatively common in some auto claims.

Why New Evidence Matters

Insurance companies generally make decisions based on the information available at the time.

When significant new evidence appears, additional review may become appropriate.

Examples include:

- Security camera footage

- Dash cam recordings

- Witness statements

- Expert reports

- Contractor evaluations

Many drivers use a VNV Front and Rear Dash Cam because video evidence may help clarify accident details that become important during claim reviews or disputes.

Security Footage Can Sometimes Change a Claim

Video evidence occasionally becomes available after a claim is closed.

Examples include footage from:

- Home security cameras

- Doorbell cameras

- Business surveillance systems

- Vehicle dash cams

Many homeowners use systems such as the Blink Outdoor Security Camera System or the Google Nest Doorbellbecause recorded footage may help document incidents involving theft, vandalism, property damage, or other losses.

Should You Contact the Insurance Company Immediately?

Generally speaking, if you discover new damage or important new information, reporting it promptly is often a good idea.

Waiting may create additional challenges.

When contacting the insurer, it may be helpful to provide:

- Claim number

- Supporting documentation

- Photographs

- Estimates

- Inspection reports

The more organized the information, the easier it may be for the insurer to review the request.

What If the Insurance Company Refuses to Reopen the Claim?

Sometimes the insurer may determine that reopening is not appropriate.

The reasons vary depending on the circumstances.

Examples may include:

- Policy limitations

- Settlement agreements

- Lack of supporting evidence

- Time-related issues

- Coverage concerns

Understanding the insurer’s reasoning is often an important first step before deciding what to do next.

Can Reopening a Claim Lead to a Dispute?

Sometimes.

Disagreements may arise regarding:

- Whether damages are related to the original loss

- Repair costs

- Coverage issues

- Claim valuation

- Evidence

When disputes occur, documentation often becomes even more important.

Strong records can help support a request for additional review.

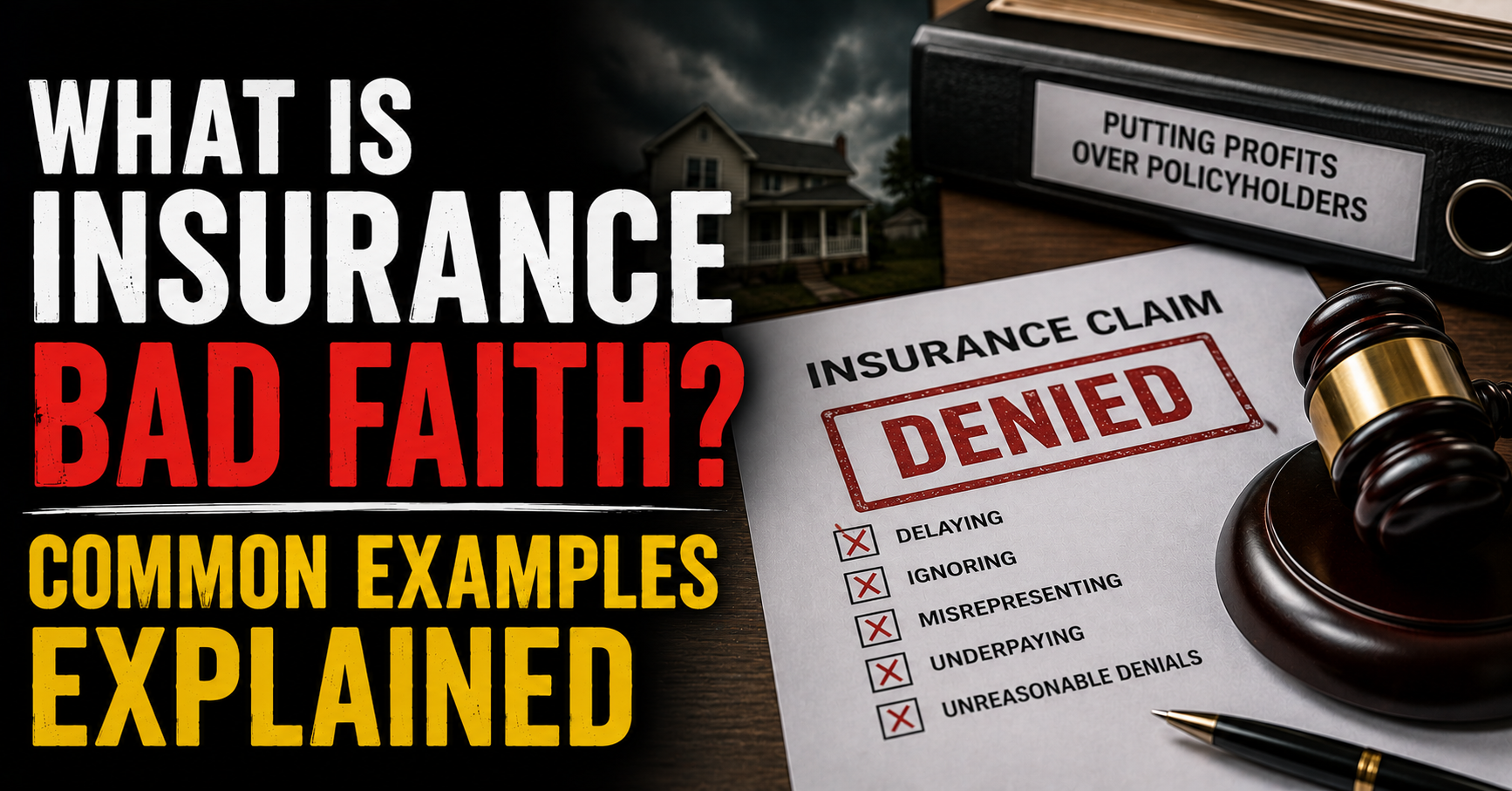

What If You Believe the Claim Was Handled Improperly?

In some situations, policyholders become concerned that the claim was not handled fairly.

Examples may include concerns regarding:

- Delays

- Communication problems

- Failure to investigate

- Denials

- Claim handling practices

If those concerns arise, these related articles may be helpful:

- Why Do Insurance Companies Delay Claims? Common Reasons

- What Is Insurance Bad Faith? Common Examples Explained

- Can You File a Complaint Against an Insurance Company?

- Can You Sue an Insurance Company?

Organized Records Can Make Reopening Easier

One of the biggest advantages a policyholder can have is complete documentation.

Helpful records often include:

- Claim files

- Estimates

- Settlement documents

- Repair invoices

- Photographs

- Correspondence

Keeping organized records can make it much easier to demonstrate why additional review may be appropriate months or even years after the original claim was closed.

Many people protect important claim records in a SentrySafe Fireproof Waterproof Document Safe or an ENGPOW Fireproof Document Storage Box while also maintaining digital backups for additional protection.

Whether a Claim Can Be Reopened Depends on the Facts

There is no universal answer that applies to every claim.

The possibility of reopening often depends on:

- The type of claim

- Policy language

- Available evidence

- New damages discovered

- Time elapsed

- Applicable state laws

Understanding these factors can help policyholders better evaluate their options when new issues arise after a claim has already been closed.

Frequently Asked Questions

Can a closed insurance claim be reopened?

Sometimes. Whether a claim can be reopened depends on factors such as the type of claim, policy language, settlement agreements, available evidence, and applicable state laws.

How long after a claim is closed can it be reopened?

There is no single deadline that applies to every insurance claim. Time limits may vary based on the policy, state law, the type of claim, and the circumstances involved.

What is a supplemental insurance claim?

A supplemental claim generally involves additional damages, costs, or information that were not included during the original claim review. Supplemental claims are common when hidden damage is discovered after repairs begin.

Can I reopen a denied insurance claim?

In some situations, yes. New evidence, corrected information, or previously unavailable documentation may sometimes lead to additional review. However, not every denied claim can be reopened.

Can hidden damage help reopen a claim?

Potentially. Hidden damage is one of the most common reasons policyholders request additional review. Supporting documentation such as contractor reports, photographs, and repair estimates is often important.

Do I need new evidence to reopen a claim?

Not always, but new evidence often strengthens a request for additional review. Examples may include photographs, videos, repair estimates, inspection reports, or witness statements.

What if the insurance company refuses to reopen my claim?

The insurer may determine that reopening is not appropriate based on policy terms, settlement agreements, available evidence, or other factors. Understanding the reason for the decision is often an important first step.

Can an insurance adjuster reinspect damage after a claim is closed?

Sometimes. Depending on the circumstances, an adjuster may be assigned to review new evidence, inspect additional damage, or evaluate supplemental repair estimates.

Can security camera footage help reopen a claim?

In some situations, yes. Newly discovered video footage may provide evidence that was unavailable during the original investigation and may support additional review.

Where can I learn more about insurance claim disputes?

You may find these related articles helpful:

- How Long Does an Insurance Claim Take? What to Expect

- What Happens After You File an Insurance Claim?

- What Happens After an Insurance Adjuster Visits?

- Can an Insurance Company Deny a Claim Without Investigation?

- What Is Insurance Bad Faith? Common Examples Explained

- Can You File a Complaint Against an Insurance Company?

- Can You Sue an Insurance Company?

- What Evidence Helps an Insurance Claim?

- What Is an Insurance Adjuster? What They Actually Do

Important Information

This article is provided for educational and informational purposes only and should not be considered legal advice. Insurance policies, claim procedures, settlement agreements, and state laws vary widely. Information provided on Legal Know It All is intended to help readers better understand insurance claims and legal concepts, not to provide legal representation or legal advice.

To learn more about how content is researched and reviewed, visit our Editorial Policy and Fact-Checking Policy pages.

Additional information about this website can be found on our About Us, Contact Us, FAQ, Disclaimer, and Terms and Conditions pages.

About the Author

Sarah Reynolds is a legal research contributor for Legal Know It All who focuses on insurance claims, consumer rights, and everyday legal issues affecting American families. She researches insurance regulations, policyholder rights, claim procedures, and consumer-focused legal topics to help readers better understand complicated subjects using plain English. Her goal is to provide trustworthy educational information that helps readers make informed decisions when dealing with insurance companies and claim disputes.

As an Amazon Associate we earn from qualifying purchases through some links in our articles. Learn more.