Filing an insurance claim is usually the easy part.

What comes next is where many people become confused.

After submitting a claim, it’s common to wonder whether you should be doing something, whether the insurance company is reviewing your case, or why nobody has called you yet. If the expected next steps do not happen, Why Do Insurance Companies Delay Claims? Common Reasons outlines common reasons a claim may appear stalled.

The good news is that most insurance claims follow a fairly predictable process.

The exact details vary depending on the type of claim, but most claims move through the same basic stages.

Understanding what happens after you file an insurance claim can help reduce stress and give you a better idea of what to expect.

Quick Answer

After you file an insurance claim, the insurance company typically opens a claim file, assigns an adjuster, investigates the loss, reviews evidence, determines coverage, and either approves, partially approves, or denies the claim. If approved, payment is issued according to the terms of the policy. The timeline can range from a few days to several months depending on the complexity of the claim. If the claim is approved but the payment seems inadequate, What Happens If an Insurance Settlement Is Too Low? addresses how policyholders may evaluate the offer.

The Insurance Company Creates a Claim File

The first thing that usually happens is the creation of a claim file.

This file becomes the central location for everything related to your claim.

It may contain:

- Photos

- Estimates

- Statements

- Police reports

- Medical records

- Inspection reports

- Emails

- Claim notes

Every communication related to the claim is generally added to this file.

You will typically receive a claim number that should be referenced whenever you contact the insurance company.

An Insurance Adjuster Is Assigned

One of the next major steps is assigning an insurance adjuster. The adjuster's responsibilities are explained in What Is an Insurance Adjuster? What They Actually Do.

The adjuster’s job is to investigate the claim and gather facts.

One of the first questions many people ask after filing a claim is how quickly the insurance company must respond. Learn more in our article on how long an insurance company has to respond to a claim.

Depending on the type of loss, the adjuster may:

- Call you

- Schedule an inspection

- Request documentation

- Review evidence

- Contact witnesses

- Review repair estimates

Some claims are handled entirely over the phone or through online submissions.

Others require in-person inspections.

After the inspection is completed, many policyholders wonder what comes next. Our article on what happens after an insurance adjuster visits explains the next stages of the claims process and what you should expect while waiting for a decision.

The Insurance Company Begins Investigating

This is often the stage where people become impatient.

From the policyholder’s perspective, it may seem like nothing is happening.

In reality, the insurance company may be reviewing a significant amount of information.

The investigation often focuses on several key questions.

What Happened?

The insurer wants to understand exactly how the loss occurred.

Is the Loss Covered?

Not every loss is covered under every policy.

Insurance companies generally review the policy language to determine whether coverage applies.

How Much Damage Exists?

The insurer must estimate the value of the loss before payment can be determined.

Is Someone Else Responsible?

In some situations another person, company, or driver may be responsible for the damages.

You May Be Asked for Additional Documents

Many people assume they have already provided everything needed when they file the claim. Knowing What Evidence Helps an Insurance Claim? can help you respond when the insurer requests additional support.

That is not always the case.

Additional documentation requests are common. A guide to What Documents Should You Keep for an Insurance Claim? can help you organize the records the insurer may need.

The insurance company may ask for:

- Photos

- Receipts

- Repair estimates

- Medical records

- Police reports

- Contractor evaluations

- Proof of ownership

Receiving a request for more information does not automatically mean there is a problem with the claim.

In many situations it is simply part of the normal investigation process.

What Happens During a Car Insurance Claim?

Vehicle claims are one of the most common types of insurance claims.

After an accident, the insurance company may:

- Review accident reports

- Examine vehicle damage

- Speak with drivers

- Contact witnesses

- Review photographs

- Analyze video evidence

If fault is disputed, the investigation may take longer.

Readers dealing with vehicle accident claims may also find helpful information in our Traffic Laws category.

Why Video Evidence Can Speed Up the Process

One of the biggest causes of claim delays is disagreement about what happened.

Imagine two drivers both claim they had a green light.

Without independent evidence, the insurer may need additional investigation.

This is one reason dash cameras have become increasingly popular.

Video footage can sometimes provide a clear record of events and help eliminate disputes.

Drivers looking to document accidents often choose products such as the VNV Front and Rear Dash Cam for Accident Evidence because it records both the front and rear of the vehicle and may help preserve valuable evidence if an accident occurs.

What Happens During a Homeowners Insurance Claim?

Homeowners claims often involve inspections.

Depending on the type of loss, the insurance company may inspect:

- Roof damage

- Water damage

- Fire damage

- Structural damage

- Personal property losses

Larger losses usually require more investigation than smaller claims.

Property owners may also find useful information in our Property Rights category.

The Insurance Company Reviews Coverage

One of the most important stages occurs when the insurer compares the facts of the claim to the policy language.

This is where the company determines:

- Whether the loss is covered

- Whether exclusions apply

- Whether policy limits affect payment

- Whether deductibles apply

This review is one reason insurance claims cannot always be resolved immediately after being reported.

The Insurance Company Makes a Decision

Eventually the insurer reaches a decision.

Generally, one of three things happens.

The Claim Is Approved

If coverage applies and the evidence supports the claim, payment may be issued according to the policy.

The Claim Is Partially Approved

Some portions of a claim may be covered while others are not.

The Claim Is Denied

If the insurer determines coverage does not apply or the claim lacks sufficient support, a denial may occur.

A denial does not automatically mean the matter is over.

Policyholders sometimes provide additional information, appeal decisions, or pursue other options.

How Long Does This Entire Process Take?

This is one of the most common questions people ask.

Unfortunately, there is no universal timeline.

Some claims move quickly.

Others take considerably longer.

If you’re wondering how long your claim may take, our article How Long Does an Insurance Claim Take? What to Expect explains common timelines, delays, and factors that affect the process.

What Should You Be Doing While the Claim Is Open?

Many policyholders worry they are not doing enough while waiting for updates.

In reality, there are several things that can help.

Save Every Document

Keep copies of:

- Emails

- Letters

- Estimates

- Receipts

- Claim numbers

- Photos

Respond Quickly

If the insurer requests information, provide it as soon as reasonably possible.

Keep Notes

Document every conversation with:

- Names

- Dates

- Times

- Topics discussed

These records can become valuable if disputes arise later.

Why Some Claims Take Longer Than Others

Several factors commonly increase claim timelines.

These include:

- Serious injuries

- Major property damage

- Disputed fault

- Multiple parties

- Missing documents

- Large weather events

- Fraud investigations

The more complicated the claim, the more investigation is generally required.

What Happens After an Insurance Adjuster Visits?

Many people assume that once the insurance adjuster visits their property or inspects their vehicle, a check is about to arrive.

Sometimes that happens.

Often, however, the adjuster’s visit is only one step in the process.

After the inspection, the adjuster may still need to:

- Review photographs

- Compare repair estimates

- Consult contractors

- Review policy language

- Submit reports to supervisors

- Request additional documentation

This is one reason some claims continue for several weeks after an inspection has already taken place.

If your adjuster recently completed an inspection, don’t panic if you don’t receive an immediate decision.

In many cases, additional review is completely normal.

What Happens If the Insurance Company Stops Communicating?

One of the most frustrating parts of any insurance claim is feeling like nobody is responding.

You leave a voicemail.

You send an email.

Days pass.

Then more days pass.

At that point, many people start wondering whether their claim has been forgotten.

While occasional delays can happen, extended periods without communication should generally be addressed.

A good first step is to politely request a status update.

Keep a record of:

- Phone calls

- Emails

- Letters

- Dates

- Names of representatives

Having a detailed record can be extremely helpful if problems develop later.

Consumers dealing with communication issues may also find useful information in our Consumer Rights category.

Can You Speed Up an Insurance Claim?

There is no magic trick that guarantees a faster claim.

However, there are several things that may help avoid unnecessary delays.

Report the Claim Quickly

The sooner the insurance company knows about the loss, the sooner the process can begin.

Take Plenty of Photos

Photos often become some of the most important evidence in a claim.

Take pictures before cleanup or repairs whenever possible.

Save Receipts

Keep receipts for:

- Repairs

- Temporary housing

- Emergency expenses

- Replacement items

These records may become important later.

Stay Organized

Many people create a folder specifically for claim documents.

Having everything in one place can save a lot of frustration.

Respond Promptly

If the insurance company requests information, try to provide it as quickly as possible.

Waiting weeks to respond can sometimes delay the claim significantly.

Why Good Evidence Can Make a Huge Difference

Insurance companies make decisions based on evidence.

The stronger your evidence, the easier it often becomes to understand what happened.

Helpful evidence may include:

- Photos

- Videos

- Police reports

- Witness statements

- Receipts

- Repair estimates

- Medical records

Vehicle accidents are a good example.

If fault is disputed, video footage can sometimes help clarify exactly what happened.

Many drivers choose to install a VNV Front and Rear Dash Cam for Accident Evidence because recorded footage may help document important events before, during, and after an accident.

While no product guarantees a favorable outcome, strong documentation can often reduce disagreements and help support a claim.

What If the Insurance Company Denies Your Claim?

Receiving a denial letter can be frustrating.

However, a denial does not automatically mean the situation is over.

In some cases:

- Additional evidence becomes available

- Documentation was missing

- Information was misunderstood

- Coverage questions remain unresolved

Some policyholders request reconsideration after providing additional information.

Others may pursue different options depending on the facts of the case and the laws in their state.

This is one reason it is important to read denial letters carefully and understand exactly why the claim was denied.

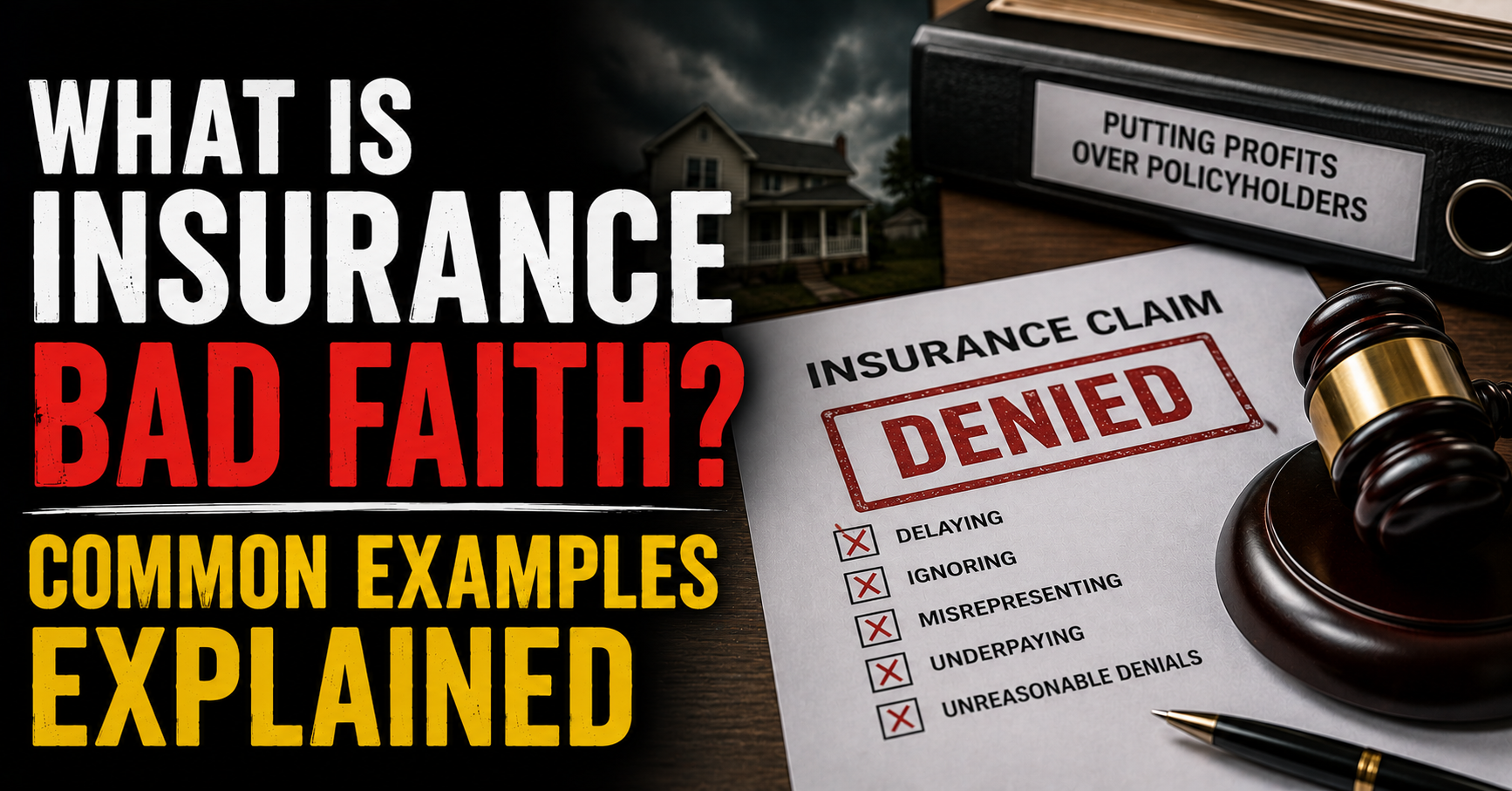

What Is Insurance Bad Faith?

You may have heard the term “insurance bad faith.”

In simple terms, bad faith generally refers to situations where an insurance company fails to meet certain obligations when handling a claim.

Examples that sometimes lead to bad faith allegations include:

- Unreasonable delays

- Failure to investigate

- Ignoring evidence

- Misrepresenting policy language

- Improper claim denials

It’s important to understand that not every denial or delay qualifies as bad faith.

Insurance bad faith laws vary significantly from state to state.

The specific facts of a claim often matter just as much as the delay itself.

Can You Sue an Insurance Company?

Sometimes.

Whether a lawsuit is possible or appropriate depends on many factors, including:

- State law

- Policy language

- Claim value

- Evidence

- The reason for the dispute

Some disagreements are resolved through negotiation.

Others may involve mediation, arbitration, or litigation.

Smaller disputes may sometimes fall within the limits of Small Claims Court, although rules vary considerably by state.

You can see our full guide on can I sue an insurance company here.

State Law Differences Matter

One of the biggest mistakes people make is assuming insurance laws work exactly the same everywhere.

They don’t.

Insurance is primarily regulated at the state level.

As a result, states may have different rules regarding:

- Claim handling requirements

- Response deadlines

- Complaint procedures

- Bad faith claims

- Settlement practices

A timeline that may be considered reasonable in one state could be viewed differently somewhere else.

Readers interested in learning more about legal differences throughout the country can visit our State Laws category.

What Should You Do While Waiting for a Claim Decision?

Waiting can be stressful.

Many people feel powerless during this stage.

The best approach is usually to stay organized and remain proactive.

Continue to:

- Save documents

- Keep communication records

- Follow up when appropriate

- Review correspondence carefully

- Respond to requests promptly

Doing these things won’t guarantee a faster outcome, but they can help prevent avoidable delays.

Understanding the Process Helps Reduce Frustration

Many insurance claims take longer than people expect.

That doesn’t necessarily mean something is wrong.

Insurance companies often need time to investigate, review evidence, inspect damage, and evaluate coverage.

Understanding each stage of the process can help you recognize the difference between a normal delay and a situation that may require additional attention.

For more educational information about claim investigations, settlements, denials, and insurance disputes, visit our Insurance Claims category.

Frequently Asked Questions

How long should it take for an insurance adjuster to contact me?

Many insurance companies contact policyholders within a few days after a claim is filed. However, the exact timeline depends on the insurer, the type of claim, and how many claims the company is handling at the time. Large storms and natural disasters can sometimes increase wait times because adjusters are dealing with a higher volume of claims.

What should I do if my insurance adjuster never calls me?

Start by contacting the insurance company directly and requesting a status update. Keep records of all phone calls, emails, and letters. If communication problems continue, you may wish to ask for a supervisor or explore complaint options available through your state’s insurance regulator.

How long does it take to receive payment after a claim is approved?

The timeline varies depending on the insurer, the type of claim, and state regulations. Some payments are issued relatively quickly after approval, while others may require additional paperwork, estimates, or processing before funds are released.

Can an insurance company ask for more documents after I already submitted everything?

Yes. It is common for insurers to request additional information during an investigation. This does not automatically mean there is a problem with your claim. In many cases, the company simply needs more information before making a final decision.

Is it normal for an insurance claim to take several months?

Sometimes. Claims involving serious injuries, major property damage, disputed liability, multiple parties, or extensive investigations often take significantly longer than straightforward claims.

Will a recorded statement affect my insurance claim?

It can. Insurance companies often use recorded statements to gather information about what happened. Before providing any statement, it is important to understand why it is being requested and answer questions honestly and accurately.

Can I repair damage before the insurance company inspects it?

In emergency situations, temporary repairs may be necessary to prevent additional damage. However, it is generally a good idea to document the damage thoroughly with photos and videos before making repairs whenever possible.

What happens if the insurance company offers less money than I expected?

Many settlement disagreements involve differing opinions about the value of damages. Depending on the circumstances, policyholders may be able to negotiate, provide additional documentation, obtain independent estimates, or explore other options.

Can an insurance company reopen an investigation after making contact?

Yes. New evidence, additional damages, conflicting information, or questions about coverage can sometimes require additional review before a final decision is made.

Where can I find more information about insurance claims?

Our Insurance Claims category contains additional educational articles covering claim timelines, denials, investigations, settlements, adjusters, consumer protections, and common insurance questions.

Additional Legal Resources

Many insurance questions overlap with other legal topics. You may also find these categories helpful:

- Insurance Claims

- Consumer Rights

- Traffic Laws

- Property Rights

- Personal Injury Law

- Small Claims Court

- State Laws

Legal Know It All is committed to publishing accurate, educational content for everyday Americans. You can learn more about how content is reviewed by visiting our Fact-Checking Policy and Editorial Policy pages.

Important Information

This article is provided for educational and informational purposes only and should not be considered legal advice. Insurance laws vary by state, insurance policies differ, and individual circumstances can significantly affect claim outcomes. Information provided on Legal Know It All is intended to help readers better understand legal concepts and insurance processes, not to provide legal representation or legal advice.

For additional information about this website and how content is created, please review our Disclaimer, Terms and Conditions, Affiliate Disclosure, and FAQ pages.

About the Author

Sarah Reynolds is a legal research contributor for Legal Know It All who focuses on insurance claims, consumer protection issues, and everyday legal questions affecting American families. She researches insurance procedures, claim handling practices, policyholder rights, and consumer-focused legal topics to help readers better understand complex subjects using plain English. Her goal is to make legal information easier to understand so readers can make informed decisions and know what questions to ask when dealing with insurance companies.

As an Amazon Associate we earn from qualifying purchases through some links in our articles. Learn more.